不知何時,香港投資者對拆細情有獨鐘,要求渣打,港交所及宏利拆細之聲此起彼落,直到宏利終於從善如流,宣布1拆2,果然創出股價一日急升50元的神話,照這個邏輯,只要1拆20,宏利股價可能翻一翻.不知這個美麗的誤會,是否港人學自內地股民,反觀海外的股東卻一點也不BUY,令宏利在海外的股價紋風不動,結果最近宏利的升幅差不多打回原形.

********

大型新股上市,必托住大市的神話,隨著中行上市又被戮破.唔知點解之前會有人信,甚至有證券行寫報告唱,大摩今次好似扮演國王的新衣的天真小孩,好既唔靈醜既靈,竟然俾佢開口中.

********

星期三, 3月 15, 2006

22/7/05 工商及科技局局長香港美國商會午餐會致辭

數 年 前 , 很 多 人 曾 談 及 固 定 及 流 動 通 訊 服 務 「 互 相 替 代 」 這 問 題 , 甚 至 有 些 人 的 想 法 , 是 流 動 服 務 可 以 作 為 單 一 的 通 訊 方 式 。 我 想 我 的 兒 子 多 年 來 也 都 是 這 樣 , 因 為 我 致 電 往 他 家 中 而 他 未 有 接 聽 時 , 他 便 是 給 我 這 個 答 案 。

在 香 港 , 流 動 通 訊 服 務 是 不 可 或 缺 的 通 訊 模 式 , 這 一 點 毋 庸 置 疑 。 本 港 的 流 動 通 訊 服 務 普 及 率 高 達 120% , 普 及 程 度 不 言 而 喻 。 事 實 上 , 部 分 人 ( 特 別 是 年 青 人 ) 以 話 音 電 話 通 訊 時 , 是 完 全 倚 賴 流 動 通 訊 服 務 的 。 我 想 很 多 企 業 用 戶 即 使 在 周 末 , 即 使 配 偶 提 出 抗 議 , 也 不 會 放 下 他 們 的 「Crackberries」。

固 網 服 務 的 發 展 也 沒 有 停 滯 不 前 。 營 辦 商 不 斷 增 加 傳 送 速 度 , 以 維 持 較 流 動 通 訊 服 務 出 色 的 優 勢 , 並 開 發 嶄 新 的 用 途 和 收 入 來 源 。 我 們 不 可 忘 記 一 點 , 就 是 流 動 通 訊 服 務 將 繼 續 倚 賴 固 網 服 務 為 傳 送 基 幹 。 其 他 固 網 服 務 營 辦 商 已 決 定 進 入 ( 香 港 最 主 要 的 固 網 商 亦 再 次 進 入 ) 流 動 通 訊 服 務 市 場 , 方 法 是 購 下 現 有 流 動 通 訊 服 務 營 辦 商 的 股 份 , 並 為 客 戶 提 供 固 網 和 流 動 通 訊 的 捆 綁 式 服 務 。

今 天 , 「 固 定 及 流 動 通 訊 服 務 互 相 替 代 」 的 看 法 , 已 變 為 一 個 嶄 新 的 概 念 - 「 固 定 及 流 動 通 訊 服 務 匯 流 」 。 這 概 念 並 非 純 粹 為 客 戶 把 固 網 和 流 動 通 訊 服 務 捆 綁 起 來 。

讓 我 向 各 位 講 一 個 例 子 。 在 英 國 , 一 名 固 網 服 務 營 辦 商 上 月 推 出 了 固 定 和 流 動 通 訊 綜 合 服 務 。 透 過 這 服 務 , 使 用 者 可 利 用 同 一 部 流 動 電 話 撥 出 或 接 聽 電 話 。 如 使 用 者 不 在 家 , 來 電 會 轉 駁 至 固 網 服 務 營 辦 商 策 略 伙 伴 的 流 動 通 訊 網 絡 。 不 過 , 如 使 用 者 在 家 , 即 使 正 在 通 話 中 , 來 電 也 會 透 過 藍 牙 或 W i - F i 連 接 技 術 及 在 使 用 者 家 中 安 裝 的 無 線 樞 紐 , 自 動 和 無 間 斷 地 轉 駁 至 固 網 服 務 營 辦 商 的 寬 頻 網 絡 , 以 善 用 固 網 服 務 更 高 質 素 、 更 穩 定 而 收 費 較 低 的 優 點 。

對 使 用 者 而 言 , 固 網 及 流 動 通 訊 網 絡 之 間 的 所 有 轉 駁 程 序 都 自 動 完 成 , 他 無 須 顧 慮 是 否 需 要 及 何 時 作 出 轉 駁 。 這 服 務 簡 單 方 便 , 不 熟 識 科 技 的 用 戶 也 可 以 使 用 。 使 用 者 無 論 在 家 中 或 到 室 外 不 同 地 方 , 通 話 也 不 會 中 斷 。 他 的 朋 友 和 客 戶 只 需 一 個 電 話 號 碼 , 便 可 與 他 聯 絡 。

這 只 是 話 音 電 話 服 務 方 面 的 例 子 。 在 本 港 , 由 於 流 動 通 訊 網 絡 覆 蓋 範 圍 甚 廣 , 且 其 通 話 計 劃 極 具 競 爭 力 , 對 一 般 的 使 用 者 來 說 , 上 述 服 務 可 能 沒 有 太 大 好 處 。 然 而 , 這 例 子 顯 示 了 電 訊 業 模 式 的 重 要 轉 變 。

今 天 , 電 訊 服 務 營 辦 商 已 不 能 再 選 擇 立 足 於 固 網 還 是 流 動 電 訊 業 , 也 不 能 按 此 分 類 來 設 計 其 服 務 計 劃 。 他 們 必 須 以 用 戶 為 中 心 , 滿 足 用 戶 ( 無 論 是 企 業 用 戶 還 是 個 別 消 費 者 ) 在 通 訊 服 務 方 面 的 需 要 。 他 們 須 高 瞻 遠 矚 , 利 用 核 心 網 絡 和 用 戶 終 端 機 方 面 的 科 技 和 標 準 匯 流 不 斷 發 展 的 優 勢 , 為 用 戶 提 供 嶄 新 和 無 間 斷 的 通 訊 服 務 。 固 定 及 流 動 電 訊 市 場 的 分 界 將 變 得 模 糊 。 電 訊 業 的 結 構 短 期 內 將 變 得 與 今 天 截 然 不 同 。

據 業 界 預 測 , 由 於 現 有 營 辦 商 轉 移 至 以 互 聯 網 規 約 為 主 的 核 心 網 絡 , 以 便 共 同 使 用 子 系 統 , 以 支 援 固 網 及 流 動 網 絡 接 收 技 術 , 因 此 固 定 及 流 動 通 訊 科 技 的 分 界 於 二 零 一 零 年 左 右 將 大 致 消 失 。 在 流 動 通 訊 網 絡 和 下 一 代 固 網 引 入 互 聯 網 規 約 多 媒 體 子 系 統 的 體 系 結 構 後 , 兩 者 的 功 能 便 會 融 合 。 如 這 預 測 準 確 , 數 年 後 , 我 們 的 通 訊 方 式 便 會 從 根 本 上 作 出 轉 變 , 成 為 無 間 斷 的 通 訊 方 式 。

政 府 的 工 作 , 是 確 保 固 定 及 流 動 通 訊 服 務 匯 流 時 , 有 關 服 務 的 轉 移 過 程 不 會 因 不 合 時 宜 的 政 策 或 較 適 用 於 舊 電 訊 服 務 模 式 的 規 例 而 受 阻 。 從 政 策 的 角 度 而 言 , 我 們 的 挑 戰 是 消 除 在 政 策 和 規 管 方 面 的 不 明 朗 因 素 , 讓 現 有 的 業 內 人 士 或 有 意 進 入 市 場 的 人 士 , 可 以 在 固 定 及 流 動 通 訊 服 務 匯 流 而 可 能 帶 來 重 大 改 變 的 時 代 , 作 出 明 智 的 投 資 決 定 。 在 這 個 迅 速 發 展 的 行 業 中 , 我 們 不 能 左 右 科 技 的 發 展 ; 我 們 只 可 維 持 科 技 中 立 的 原 則 , 讓 市 場 力 量 來 決 定 最 適 當 的 技 術 和 標 準 , 以 切 合 用 戶 的 需 求 。 提 供 可 用 於 這 些 新 無 線 科 技 上 的 無 線 電 頻 譜 , 是 當 局 另 一 項 重 要 的 政 策 事 宜 。 我 們 將 於 檢 討 頻 譜 政 策 時 , 一 併 考 慮 這 事 。

在 規 管 方 面 , 電 訊 管 理 局 將 聘 請 專 家 , 協 助 我 們 檢 討 有 關 固 定 及 流 動 通 訊 服 務 匯 流 的 事 宜 。 我 希 望 與 各 位 談 談 這 次 檢 討 工 作 所 涉 及 的 三 項 事 宜 。

首 項 須 研 究 的 議 題 是 關 於 傳 送 者 牌 照 的 發 牌 安 排 。 在 我 們 現 行 發 牌 制 度 內 , 固 定 及 流 動 電 訊 傳 送 者 分 界 清 晰 , 各 有 相 應 的 權 利 及 義 務 。 舉 例 來 說 , 固 定 電 訊 傳 送 者 有 權 敷 設 電 纜 , 並 使 用 大 廈 內 的 設 施 以 接 達 用 戶 ; 流 動 電 訊 傳 送 者 則 獲 指 配 無 線 電 頻 譜 , 提 供 服 務 地 點 不 限 。 固 定 及 流 動 電 訊 服 務 匯 流 後 , 若 干 服 務 可 能 會 界 乎 固 定 及 流 動 電 訊 服 務 之 間 。 我 們 早 前 建 議 對 寬 頻 無 線 接 達 服 務(BWA)發 牌 , 便 是 其 中 一 個 例 子 。

全 球 微 波 接 入 互 通 作 業 系 統(WiMAX)已 發 展 了 若 干 流 動 通 訊 標 準 , 數 年 間 便 可 以 商 業 形 式 運 作 。 業 內 部 分 人 士 現 正 爭 議 , 謂 B W A 並 非 固 定 電 訊 服 務 ; 目 前 也 許 還 是 固 定 電 訊 服 務 , 但 數 年 後 一 定 不 是 。 另 一 方 面 , 某 些 較 為 人 熟 悉 的 B W A 標 準 與 目 前 的 流 動 電 訊 服 務 不 同 , 尚 未 能 提 供 樞 紐 與 樞 紐 之 間 的 無 間 斷 自 動 轉 接 。 因 此 , 對 用 戶 來 說 , BWA 服 務 的 「 流 動 性 」 並 不 及 今 天 的 第 二 代 及 第 三 代 流 動 電 訊 服 務 。

我 們 需 要 考 慮 的 , 是 我 們 是 否 須 制 訂 一 類 新 牌 照 , 例 如 「 統 一 服 務 」 傳 送 者 牌 照 。 我 們 需 要 考 慮 這 類 新 「 統 一 服 務 」 傳 送 者 牌 照 須 設 定 何 種 權 利 及 義 務 。 我 們 也 需 要 考 慮 是 否 讓 現 有 的 固 定 及 流 動 電 訊 傳 送 者 牌 照 持 有 人 轉 移 至 持 有 這 類 新 「 統 一 服 務 」 傳 送 者 牌 照 ; 如 果 是 的 話 , 要 有 怎 樣 的 適 當 過 渡 安 排 。

第 二 項 須 研 究 的 議 題 , 是 固 定 與 流 動 電 訊 傳 送 者 之 間 的 互 連 收 費 安 排 。 這 是 流 動 電 訊 服 務 營 辦 商 已 多 次 提 出 的 問 題 。

在 電 路 交 換 網 下 , 各 網 絡 須 作 互 連 , 以 便 來 電 者 在 某 一 網 絡 上 的 電 話 通 話 可 發 送 至 另 一 網 絡 上 的 接 電 者 。 當 一 個 網 絡 使 用 另 一 個 網 絡 的 資 源 來 完 成 互 連 時 , 來 電 的 網 絡 ( 始 發 網 絡 ) 營 辦 商 或 須 向 接 電 的 網 絡 ( 終 端 網 絡 ) 營 辦 商 提 供 若 干 補 償 。

本 港 採 用 所 謂 「 流 動 一 方 付 費 」 的 用 戶 收 費 安 排 。 由 於 流 動 電 訊 服 務 用 戶 支 付 他 所 撥 出 和 接 聽 電 話 通 話 的 費 用 , 流 動 電 訊 網 絡 營 辦 商 遂 向 固 定 電 訊 網 絡 營 辦 商 支 付 互 連 費 用 , 不 論 該 通 話 是 撥 出 還 是 接 聽 。 這 項 安 排 早 於 八 十 年 代 流 動 電 訊 服 務 引 進 之 初 便 已 實 施 。

另 一 項 用 戶 收 費 安 排 是 所 謂 「 來 電 一 方 付 費 」 。 由 於 用 戶 只 支 付 他 所 撥 出 電 話 的 費 用 , 而 他 所 支 付 的 費 用 已 包 括 把 通 話 發 送 至 對 方 全 程 所 需 的 一 切 費 用 , 故 來 電 網 絡 的 營 辦 商 向 接 電 網 絡 的 營 辦 商 支 付 互 連 費 用 。 在 其 他 國 家 , 當 固 網 互 連 至 流 動 網 絡 時 , 便 會 採 用 這 項 做 法 。 在 本 港 , 只 有 當 固 網 互 連 至 固 網 時 , 才 會 採 用 這 項 做 法 。

第 三 項 安 排 稱 為 「 發 送 一 方 得 全 費 」 。 互 連 的 網 絡 使 用 接 電 者 的 網 絡 後 , 不 會 向 對 方 支 付 補 償 費 , 並 可 保 留 所 有 從 來 電 用 戶 處 收 取 的 收 入 。 本 港 的 流 動 電 訊 服 務 營 辦 商 在 互 連 時 採 用 這 項 安 排 。

雖 然 這 項 互 連 收 費 安 排 看 起 來 可 能 是 小 圈 子 的 事 , 但 此 事 在 業 內 仍 是 重 要 議 程 , 因 為 這 涉 及 大 量 金 錢 。 舉 例 來 說 , 在 目 前 非 對 等 互 連 收 費 制 度 下 , 本 港 的 固 網 電 訊 營 辦 商 每 年 可 收 取 數 以 億 計 的 互 連 費 用 , 視 乎 在 其 網 絡 上 終 結 的 流 動 通 訊 量 而 定 。

互 連 收 費 安 排 並 無 對 錯 可 言 , 因 為 同 一 市 場 內 的 營 辦 商 遵 從 同 一 安 排 。 最 重 要 的 是 , 他 們 在 公 平 情 況 下 競 爭 。

部 分 流 動 電 訊 服 務 營 辦 商 聲 稱 「 流 動 一 方 付 費 」 及 相 關 的 非 對 等 互 連 收 費 制 度 兩 項 因 素 , 在 本 港 造 成 商 戶 未 經 流 動 電 話 用 戶 許 可 便 向 其 撥 出 直 銷 電 話 的 問 題 。 這 是 因 為 從 固 網 電 話 撥 出 電 話 通 話 越 多 , 固 網 電 訊 服 務 營 辦 商 向 流 動 電 訊 服 務 營 辦 商 收 取 的 互 連 費 用 便 越 多 。

對 這 個 說 法 , 我 沒 有 足 夠 的 實 證 可 作 判 斷 。 不 過 , 目 前 的 互 連 收 費 安 排 顯 然 須 予 檢 討 , 為 日 後 固 定 及 流 動 電 訊 服 務 匯 流 作 好 準 備 。 我 們 為 打 擊 濫 發 訊 息 而 推 出 的 一 籃 子 措 施 中 , 正 為 此 作 進 一 步 研 究 。

第 三 項 須 研 究 的 議 題 , 是 固 網 與 流 動 網 絡 之 間 的 電 話 號 碼 可 攜 服 務 。 除 特 別 的 接 入 號 碼 外 , 本 港 目 前 的 固 網 電 話 號 碼 以 「 2 」 或 「 3 」 字 為 首 , 流 動 電 話 號 碼 則 以 「 6 」 或 「 9 」 字 為 首 。

在 此 固 定 及 流 動 電 訊 服 務 匯 流 的 世 代 中 , 兩 種 服 務 的 界 線 變 得 模 糊 , 再 也 不 能 簡 單 地 純 以 一 個 電 話 號 碼 來 界 定 這 會 由 固 網 還 是 流 動 網 絡 接 駁 。 不 過 , 讓 電 話 號 碼 在 固 網 與 流 動 網 絡 之 間 轉 移 , 可 令 部 分 以 電 話 號 碼 來 分 辦 來 電 者 屬 哪 一 種 網 絡 的 現 行 安 排 產 生 問 題 。 互 連 收 費 安 排 便 是 一 個 重 要 例 子 。 我 們 須 處 理 這 個 電 話 號 碼 可 攜 性 問 題 。

各 位 來 賓 , 我 們 的 電 訊 市 場 現 正 處 於 一 個 令 人 神 迷 的 時 刻 。 過 去 十 年 , 本 港 電 訊 市 場 開 放 , 成 績 美 滿 , 新 加 入 市 場 的 營 辦 商 令 用 戶 的 收 費 大 幅 下 降 。 我 們 即 將 見 證 電 訊 業 的 另 一 項 重 大 發 展 。 我 們 須 堅 守 本 位 , 令 我 們 的 政 策 及 規 管 架 構 能 配 合 這 項 發 展 。

電 訊 管 理 局 短 期 內 會 委 託 顧 問 公 司 , 就 與 規 管 架 構 有 關 的 事 宜 進 行 研 究 , 詳 細 探 討 經 濟 效 益 及 成 本 效 益 分 析 。 研 究 會 以 其 他 規 管 架 構 為 基 準 、 評 估 本 港 的 市 場 形 勢 、 向 業 內 人 士 蒐 集 意 見 並 予 分 析 , 以 及 根 據 成 本 效 益 分 析 提 出 適 當 的 變 革 建 議 。 希 望 顧 問 研 究 能 為 我 們 提 供 穩 固 的 基 礎 , 讓 我 們 於 今 年 稍 後 , 就 固 定 及 流 動 電 訊 服 務 匯 流 一 事 諮 詢 公 眾 。

在 香 港 , 流 動 通 訊 服 務 是 不 可 或 缺 的 通 訊 模 式 , 這 一 點 毋 庸 置 疑 。 本 港 的 流 動 通 訊 服 務 普 及 率 高 達 120% , 普 及 程 度 不 言 而 喻 。 事 實 上 , 部 分 人 ( 特 別 是 年 青 人 ) 以 話 音 電 話 通 訊 時 , 是 完 全 倚 賴 流 動 通 訊 服 務 的 。 我 想 很 多 企 業 用 戶 即 使 在 周 末 , 即 使 配 偶 提 出 抗 議 , 也 不 會 放 下 他 們 的 「Crackberries」。

固 網 服 務 的 發 展 也 沒 有 停 滯 不 前 。 營 辦 商 不 斷 增 加 傳 送 速 度 , 以 維 持 較 流 動 通 訊 服 務 出 色 的 優 勢 , 並 開 發 嶄 新 的 用 途 和 收 入 來 源 。 我 們 不 可 忘 記 一 點 , 就 是 流 動 通 訊 服 務 將 繼 續 倚 賴 固 網 服 務 為 傳 送 基 幹 。 其 他 固 網 服 務 營 辦 商 已 決 定 進 入 ( 香 港 最 主 要 的 固 網 商 亦 再 次 進 入 ) 流 動 通 訊 服 務 市 場 , 方 法 是 購 下 現 有 流 動 通 訊 服 務 營 辦 商 的 股 份 , 並 為 客 戶 提 供 固 網 和 流 動 通 訊 的 捆 綁 式 服 務 。

今 天 , 「 固 定 及 流 動 通 訊 服 務 互 相 替 代 」 的 看 法 , 已 變 為 一 個 嶄 新 的 概 念 - 「 固 定 及 流 動 通 訊 服 務 匯 流 」 。 這 概 念 並 非 純 粹 為 客 戶 把 固 網 和 流 動 通 訊 服 務 捆 綁 起 來 。

讓 我 向 各 位 講 一 個 例 子 。 在 英 國 , 一 名 固 網 服 務 營 辦 商 上 月 推 出 了 固 定 和 流 動 通 訊 綜 合 服 務 。 透 過 這 服 務 , 使 用 者 可 利 用 同 一 部 流 動 電 話 撥 出 或 接 聽 電 話 。 如 使 用 者 不 在 家 , 來 電 會 轉 駁 至 固 網 服 務 營 辦 商 策 略 伙 伴 的 流 動 通 訊 網 絡 。 不 過 , 如 使 用 者 在 家 , 即 使 正 在 通 話 中 , 來 電 也 會 透 過 藍 牙 或 W i - F i 連 接 技 術 及 在 使 用 者 家 中 安 裝 的 無 線 樞 紐 , 自 動 和 無 間 斷 地 轉 駁 至 固 網 服 務 營 辦 商 的 寬 頻 網 絡 , 以 善 用 固 網 服 務 更 高 質 素 、 更 穩 定 而 收 費 較 低 的 優 點 。

對 使 用 者 而 言 , 固 網 及 流 動 通 訊 網 絡 之 間 的 所 有 轉 駁 程 序 都 自 動 完 成 , 他 無 須 顧 慮 是 否 需 要 及 何 時 作 出 轉 駁 。 這 服 務 簡 單 方 便 , 不 熟 識 科 技 的 用 戶 也 可 以 使 用 。 使 用 者 無 論 在 家 中 或 到 室 外 不 同 地 方 , 通 話 也 不 會 中 斷 。 他 的 朋 友 和 客 戶 只 需 一 個 電 話 號 碼 , 便 可 與 他 聯 絡 。

這 只 是 話 音 電 話 服 務 方 面 的 例 子 。 在 本 港 , 由 於 流 動 通 訊 網 絡 覆 蓋 範 圍 甚 廣 , 且 其 通 話 計 劃 極 具 競 爭 力 , 對 一 般 的 使 用 者 來 說 , 上 述 服 務 可 能 沒 有 太 大 好 處 。 然 而 , 這 例 子 顯 示 了 電 訊 業 模 式 的 重 要 轉 變 。

今 天 , 電 訊 服 務 營 辦 商 已 不 能 再 選 擇 立 足 於 固 網 還 是 流 動 電 訊 業 , 也 不 能 按 此 分 類 來 設 計 其 服 務 計 劃 。 他 們 必 須 以 用 戶 為 中 心 , 滿 足 用 戶 ( 無 論 是 企 業 用 戶 還 是 個 別 消 費 者 ) 在 通 訊 服 務 方 面 的 需 要 。 他 們 須 高 瞻 遠 矚 , 利 用 核 心 網 絡 和 用 戶 終 端 機 方 面 的 科 技 和 標 準 匯 流 不 斷 發 展 的 優 勢 , 為 用 戶 提 供 嶄 新 和 無 間 斷 的 通 訊 服 務 。 固 定 及 流 動 電 訊 市 場 的 分 界 將 變 得 模 糊 。 電 訊 業 的 結 構 短 期 內 將 變 得 與 今 天 截 然 不 同 。

據 業 界 預 測 , 由 於 現 有 營 辦 商 轉 移 至 以 互 聯 網 規 約 為 主 的 核 心 網 絡 , 以 便 共 同 使 用 子 系 統 , 以 支 援 固 網 及 流 動 網 絡 接 收 技 術 , 因 此 固 定 及 流 動 通 訊 科 技 的 分 界 於 二 零 一 零 年 左 右 將 大 致 消 失 。 在 流 動 通 訊 網 絡 和 下 一 代 固 網 引 入 互 聯 網 規 約 多 媒 體 子 系 統 的 體 系 結 構 後 , 兩 者 的 功 能 便 會 融 合 。 如 這 預 測 準 確 , 數 年 後 , 我 們 的 通 訊 方 式 便 會 從 根 本 上 作 出 轉 變 , 成 為 無 間 斷 的 通 訊 方 式 。

政 府 的 工 作 , 是 確 保 固 定 及 流 動 通 訊 服 務 匯 流 時 , 有 關 服 務 的 轉 移 過 程 不 會 因 不 合 時 宜 的 政 策 或 較 適 用 於 舊 電 訊 服 務 模 式 的 規 例 而 受 阻 。 從 政 策 的 角 度 而 言 , 我 們 的 挑 戰 是 消 除 在 政 策 和 規 管 方 面 的 不 明 朗 因 素 , 讓 現 有 的 業 內 人 士 或 有 意 進 入 市 場 的 人 士 , 可 以 在 固 定 及 流 動 通 訊 服 務 匯 流 而 可 能 帶 來 重 大 改 變 的 時 代 , 作 出 明 智 的 投 資 決 定 。 在 這 個 迅 速 發 展 的 行 業 中 , 我 們 不 能 左 右 科 技 的 發 展 ; 我 們 只 可 維 持 科 技 中 立 的 原 則 , 讓 市 場 力 量 來 決 定 最 適 當 的 技 術 和 標 準 , 以 切 合 用 戶 的 需 求 。 提 供 可 用 於 這 些 新 無 線 科 技 上 的 無 線 電 頻 譜 , 是 當 局 另 一 項 重 要 的 政 策 事 宜 。 我 們 將 於 檢 討 頻 譜 政 策 時 , 一 併 考 慮 這 事 。

在 規 管 方 面 , 電 訊 管 理 局 將 聘 請 專 家 , 協 助 我 們 檢 討 有 關 固 定 及 流 動 通 訊 服 務 匯 流 的 事 宜 。 我 希 望 與 各 位 談 談 這 次 檢 討 工 作 所 涉 及 的 三 項 事 宜 。

首 項 須 研 究 的 議 題 是 關 於 傳 送 者 牌 照 的 發 牌 安 排 。 在 我 們 現 行 發 牌 制 度 內 , 固 定 及 流 動 電 訊 傳 送 者 分 界 清 晰 , 各 有 相 應 的 權 利 及 義 務 。 舉 例 來 說 , 固 定 電 訊 傳 送 者 有 權 敷 設 電 纜 , 並 使 用 大 廈 內 的 設 施 以 接 達 用 戶 ; 流 動 電 訊 傳 送 者 則 獲 指 配 無 線 電 頻 譜 , 提 供 服 務 地 點 不 限 。 固 定 及 流 動 電 訊 服 務 匯 流 後 , 若 干 服 務 可 能 會 界 乎 固 定 及 流 動 電 訊 服 務 之 間 。 我 們 早 前 建 議 對 寬 頻 無 線 接 達 服 務(BWA)發 牌 , 便 是 其 中 一 個 例 子 。

全 球 微 波 接 入 互 通 作 業 系 統(WiMAX)已 發 展 了 若 干 流 動 通 訊 標 準 , 數 年 間 便 可 以 商 業 形 式 運 作 。 業 內 部 分 人 士 現 正 爭 議 , 謂 B W A 並 非 固 定 電 訊 服 務 ; 目 前 也 許 還 是 固 定 電 訊 服 務 , 但 數 年 後 一 定 不 是 。 另 一 方 面 , 某 些 較 為 人 熟 悉 的 B W A 標 準 與 目 前 的 流 動 電 訊 服 務 不 同 , 尚 未 能 提 供 樞 紐 與 樞 紐 之 間 的 無 間 斷 自 動 轉 接 。 因 此 , 對 用 戶 來 說 , BWA 服 務 的 「 流 動 性 」 並 不 及 今 天 的 第 二 代 及 第 三 代 流 動 電 訊 服 務 。

我 們 需 要 考 慮 的 , 是 我 們 是 否 須 制 訂 一 類 新 牌 照 , 例 如 「 統 一 服 務 」 傳 送 者 牌 照 。 我 們 需 要 考 慮 這 類 新 「 統 一 服 務 」 傳 送 者 牌 照 須 設 定 何 種 權 利 及 義 務 。 我 們 也 需 要 考 慮 是 否 讓 現 有 的 固 定 及 流 動 電 訊 傳 送 者 牌 照 持 有 人 轉 移 至 持 有 這 類 新 「 統 一 服 務 」 傳 送 者 牌 照 ; 如 果 是 的 話 , 要 有 怎 樣 的 適 當 過 渡 安 排 。

第 二 項 須 研 究 的 議 題 , 是 固 定 與 流 動 電 訊 傳 送 者 之 間 的 互 連 收 費 安 排 。 這 是 流 動 電 訊 服 務 營 辦 商 已 多 次 提 出 的 問 題 。

在 電 路 交 換 網 下 , 各 網 絡 須 作 互 連 , 以 便 來 電 者 在 某 一 網 絡 上 的 電 話 通 話 可 發 送 至 另 一 網 絡 上 的 接 電 者 。 當 一 個 網 絡 使 用 另 一 個 網 絡 的 資 源 來 完 成 互 連 時 , 來 電 的 網 絡 ( 始 發 網 絡 ) 營 辦 商 或 須 向 接 電 的 網 絡 ( 終 端 網 絡 ) 營 辦 商 提 供 若 干 補 償 。

本 港 採 用 所 謂 「 流 動 一 方 付 費 」 的 用 戶 收 費 安 排 。 由 於 流 動 電 訊 服 務 用 戶 支 付 他 所 撥 出 和 接 聽 電 話 通 話 的 費 用 , 流 動 電 訊 網 絡 營 辦 商 遂 向 固 定 電 訊 網 絡 營 辦 商 支 付 互 連 費 用 , 不 論 該 通 話 是 撥 出 還 是 接 聽 。 這 項 安 排 早 於 八 十 年 代 流 動 電 訊 服 務 引 進 之 初 便 已 實 施 。

另 一 項 用 戶 收 費 安 排 是 所 謂 「 來 電 一 方 付 費 」 。 由 於 用 戶 只 支 付 他 所 撥 出 電 話 的 費 用 , 而 他 所 支 付 的 費 用 已 包 括 把 通 話 發 送 至 對 方 全 程 所 需 的 一 切 費 用 , 故 來 電 網 絡 的 營 辦 商 向 接 電 網 絡 的 營 辦 商 支 付 互 連 費 用 。 在 其 他 國 家 , 當 固 網 互 連 至 流 動 網 絡 時 , 便 會 採 用 這 項 做 法 。 在 本 港 , 只 有 當 固 網 互 連 至 固 網 時 , 才 會 採 用 這 項 做 法 。

第 三 項 安 排 稱 為 「 發 送 一 方 得 全 費 」 。 互 連 的 網 絡 使 用 接 電 者 的 網 絡 後 , 不 會 向 對 方 支 付 補 償 費 , 並 可 保 留 所 有 從 來 電 用 戶 處 收 取 的 收 入 。 本 港 的 流 動 電 訊 服 務 營 辦 商 在 互 連 時 採 用 這 項 安 排 。

雖 然 這 項 互 連 收 費 安 排 看 起 來 可 能 是 小 圈 子 的 事 , 但 此 事 在 業 內 仍 是 重 要 議 程 , 因 為 這 涉 及 大 量 金 錢 。 舉 例 來 說 , 在 目 前 非 對 等 互 連 收 費 制 度 下 , 本 港 的 固 網 電 訊 營 辦 商 每 年 可 收 取 數 以 億 計 的 互 連 費 用 , 視 乎 在 其 網 絡 上 終 結 的 流 動 通 訊 量 而 定 。

互 連 收 費 安 排 並 無 對 錯 可 言 , 因 為 同 一 市 場 內 的 營 辦 商 遵 從 同 一 安 排 。 最 重 要 的 是 , 他 們 在 公 平 情 況 下 競 爭 。

部 分 流 動 電 訊 服 務 營 辦 商 聲 稱 「 流 動 一 方 付 費 」 及 相 關 的 非 對 等 互 連 收 費 制 度 兩 項 因 素 , 在 本 港 造 成 商 戶 未 經 流 動 電 話 用 戶 許 可 便 向 其 撥 出 直 銷 電 話 的 問 題 。 這 是 因 為 從 固 網 電 話 撥 出 電 話 通 話 越 多 , 固 網 電 訊 服 務 營 辦 商 向 流 動 電 訊 服 務 營 辦 商 收 取 的 互 連 費 用 便 越 多 。

對 這 個 說 法 , 我 沒 有 足 夠 的 實 證 可 作 判 斷 。 不 過 , 目 前 的 互 連 收 費 安 排 顯 然 須 予 檢 討 , 為 日 後 固 定 及 流 動 電 訊 服 務 匯 流 作 好 準 備 。 我 們 為 打 擊 濫 發 訊 息 而 推 出 的 一 籃 子 措 施 中 , 正 為 此 作 進 一 步 研 究 。

第 三 項 須 研 究 的 議 題 , 是 固 網 與 流 動 網 絡 之 間 的 電 話 號 碼 可 攜 服 務 。 除 特 別 的 接 入 號 碼 外 , 本 港 目 前 的 固 網 電 話 號 碼 以 「 2 」 或 「 3 」 字 為 首 , 流 動 電 話 號 碼 則 以 「 6 」 或 「 9 」 字 為 首 。

在 此 固 定 及 流 動 電 訊 服 務 匯 流 的 世 代 中 , 兩 種 服 務 的 界 線 變 得 模 糊 , 再 也 不 能 簡 單 地 純 以 一 個 電 話 號 碼 來 界 定 這 會 由 固 網 還 是 流 動 網 絡 接 駁 。 不 過 , 讓 電 話 號 碼 在 固 網 與 流 動 網 絡 之 間 轉 移 , 可 令 部 分 以 電 話 號 碼 來 分 辦 來 電 者 屬 哪 一 種 網 絡 的 現 行 安 排 產 生 問 題 。 互 連 收 費 安 排 便 是 一 個 重 要 例 子 。 我 們 須 處 理 這 個 電 話 號 碼 可 攜 性 問 題 。

各 位 來 賓 , 我 們 的 電 訊 市 場 現 正 處 於 一 個 令 人 神 迷 的 時 刻 。 過 去 十 年 , 本 港 電 訊 市 場 開 放 , 成 績 美 滿 , 新 加 入 市 場 的 營 辦 商 令 用 戶 的 收 費 大 幅 下 降 。 我 們 即 將 見 證 電 訊 業 的 另 一 項 重 大 發 展 。 我 們 須 堅 守 本 位 , 令 我 們 的 政 策 及 規 管 架 構 能 配 合 這 項 發 展 。

電 訊 管 理 局 短 期 內 會 委 託 顧 問 公 司 , 就 與 規 管 架 構 有 關 的 事 宜 進 行 研 究 , 詳 細 探 討 經 濟 效 益 及 成 本 效 益 分 析 。 研 究 會 以 其 他 規 管 架 構 為 基 準 、 評 估 本 港 的 市 場 形 勢 、 向 業 內 人 士 蒐 集 意 見 並 予 分 析 , 以 及 根 據 成 本 效 益 分 析 提 出 適 當 的 變 革 建 議 。 希 望 顧 問 研 究 能 為 我 們 提 供 穩 固 的 基 礎 , 讓 我 們 於 今 年 稍 後 , 就 固 定 及 流 動 電 訊 服 務 匯 流 一 事 諮 詢 公 眾 。

星期五, 2月 24, 2006

星期四, 12月 29, 2005

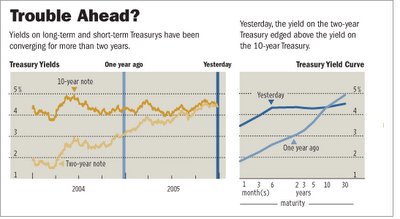

Inverse yield curve

Yields on Bonds Invert, ReflectingUnease About Economy's Future

By MARK WHITEHOUSE

Staff Reporter of THE WALL STREET JOURNAL

December 28, 2005

The nation's bond market interrupted the holiday season with a downbeat message yesterday: Many investors expect the economy to hit tougher times within the next year or so.

That pronouncement came in the form of long-term interest rates dropping below short-term rates, a trend that often -- but not always -- precedes an economic downturn. The development is known as an inversion, because it flips the traditionally upward-sloping shape of bond yields plotted on a graph. The yield curve typically rises because longer-term debt usually pays higher interest rates to compensate investor s for the greater risk they incur waiting for repayment.

s for the greater risk they incur waiting for repayment.

Inversions can squeeze or even eliminate profit margins for banks, hedge funds and any other financial business that borrows money at short-term rates and lends it at long-term rates. "This is a warning signal...that we are on recession watch now," says Paul Kasriel, chief economist at Northern Trust Co. in Chicago. The inversion, however, so far is minor, he says. And some economists believe an inversion isn't as reliable a predictor as it once was.

In late New York trading, the yield on the 10-year Treasury note, which reflects investors' long-term view of the economy and is a key benchmark for mortgage loans, had dropped just slightly below the yield on the two-year note, which tracks expectations for the Federal Reserve's monetary policy in the nearer term. The 10-year note's price was up ¼ point, or $2.50 for each $1,000 in face value, to yield 4.343%. The two-year note was up 1/32 point to yield 4.347%, and the 30-year bond was up 21/32 to yield 4.508%.

The bond market's gloom may seem incongruous, given that inflation remains under control and the economy grew at an annual rate of 4.1% in the third quarter, marking the eighth straight quarter of one of the most stable stretches of growth on record. Analysts cautioned against reading too much into the timing of the inversion, which came amid a dearth of economic or other market-moving news and amid thin holiday dealings. Still, it was the first inversion in five years, and many see it as a signal of bigger, sustained moves to come. It was also cited as a factor behind a weaker stock market yesterday. (See related article.)

"The big question is how dramatic [the inversion] becomes," says Thomas Girard, co-head of fixed income at Weiss Peck & Greer Investments in New York.

Bonds make fixed interest and principal payments to investors, but their yield depends on what the market is willing to pay for the bonds on any given day. In deciding what yield -- or return -- to demand on bonds, investors consider various factors, including their expectations for future short-term interest rates and the bond's duration.

Investors, for example, usually demand more yield from governments and companies to tie up their money in longer-term bonds. When they are willing to accept a lower yield, that means they are persuaded that the Fed, which most expect to raise short-term rates to 4.5% or higher early next year, will soon have to bring those rates back down to mitigate, or ward off, a recession. Yield-curve inversions have preceded all of the last six recessions, but have also sounded two false alarms, the most recent in 1998.

The housing market is the most likely trigger for an economic slowdown and Fed reversal. As the Fed raises rates, monthly payments on adjustable-rate home loans go up, cooling demand for houses and leaving homeowners with less money to spend on all the other things companies want to sell them. Second, as house prices stall, homeowners aren't able to borrow as much against the value of their homes -- a source of cash that has added hundreds of billions of dollars to consumers' spending power in recent years.

"What the Fed is going to do is shut down the ATM machine known as the housing market," says Tad Rivelle, chief investment officer at Metropolitan West Asset Management in Los Angeles. Fed policy makers hold their next meeting on Jan. 31, which is expected to be the last before Chairman Alan Greenspan retires, leaving the reins to Ben Bernanke, the nominee to succeed him.

The Fed's attempts to cool the economy, however, don't always provoke a recession, and many economists, including Mr. Greenspan, suggest that the yield curve might have lost its predictive abilities. That's because foreign buying of U.S. Treasurys and the Fed's success in controlling inflation have kept long-term interest rates unusually low, so U.S. consumers and companies still have relatively cheap access to money that they can spend on buying houses and building factories.

A recent study published by the Fed estimated that in the absence of foreign buying, the difference between two-year and 10-year yields would be about 0.75 percentage point greater.

"Many factors can affect the slope of the yield curve, and these factors do not all have the same implications for future output growth," Mr. Greenspan wrote in a recent letter to Congress.

But even if it doesn't presage recession, a severe and prolonged inversion can cause a lot of pain, particularly for banks and hedge funds that make long-term investments with money borrowed at short-term rates -- the so-called carry trade. Big banks such as Citigroup Inc.'s Citibank unit and J.P. Morgan Chase & Co. have already cited the flattening yield curve as a factor affecting profits, as the interest rate they must pay to attract deposits rises closer to the return they can expect on their investments. "You can't make it up on volume if you're borrowing at 4.25% and lending at 4%," Northern Trust's Mr. Kasriel says.

By MARK WHITEHOUSE

Staff Reporter of THE WALL STREET JOURNAL

December 28, 2005

The nation's bond market interrupted the holiday season with a downbeat message yesterday: Many investors expect the economy to hit tougher times within the next year or so.

That pronouncement came in the form of long-term interest rates dropping below short-term rates, a trend that often -- but not always -- precedes an economic downturn. The development is known as an inversion, because it flips the traditionally upward-sloping shape of bond yields plotted on a graph. The yield curve typically rises because longer-term debt usually pays higher interest rates to compensate investor

s for the greater risk they incur waiting for repayment.

s for the greater risk they incur waiting for repayment.Inversions can squeeze or even eliminate profit margins for banks, hedge funds and any other financial business that borrows money at short-term rates and lends it at long-term rates. "This is a warning signal...that we are on recession watch now," says Paul Kasriel, chief economist at Northern Trust Co. in Chicago. The inversion, however, so far is minor, he says. And some economists believe an inversion isn't as reliable a predictor as it once was.

In late New York trading, the yield on the 10-year Treasury note, which reflects investors' long-term view of the economy and is a key benchmark for mortgage loans, had dropped just slightly below the yield on the two-year note, which tracks expectations for the Federal Reserve's monetary policy in the nearer term. The 10-year note's price was up ¼ point, or $2.50 for each $1,000 in face value, to yield 4.343%. The two-year note was up 1/32 point to yield 4.347%, and the 30-year bond was up 21/32 to yield 4.508%.

The bond market's gloom may seem incongruous, given that inflation remains under control and the economy grew at an annual rate of 4.1% in the third quarter, marking the eighth straight quarter of one of the most stable stretches of growth on record. Analysts cautioned against reading too much into the timing of the inversion, which came amid a dearth of economic or other market-moving news and amid thin holiday dealings. Still, it was the first inversion in five years, and many see it as a signal of bigger, sustained moves to come. It was also cited as a factor behind a weaker stock market yesterday. (See related article.)

"The big question is how dramatic [the inversion] becomes," says Thomas Girard, co-head of fixed income at Weiss Peck & Greer Investments in New York.

Bonds make fixed interest and principal payments to investors, but their yield depends on what the market is willing to pay for the bonds on any given day. In deciding what yield -- or return -- to demand on bonds, investors consider various factors, including their expectations for future short-term interest rates and the bond's duration.

Investors, for example, usually demand more yield from governments and companies to tie up their money in longer-term bonds. When they are willing to accept a lower yield, that means they are persuaded that the Fed, which most expect to raise short-term rates to 4.5% or higher early next year, will soon have to bring those rates back down to mitigate, or ward off, a recession. Yield-curve inversions have preceded all of the last six recessions, but have also sounded two false alarms, the most recent in 1998.

The housing market is the most likely trigger for an economic slowdown and Fed reversal. As the Fed raises rates, monthly payments on adjustable-rate home loans go up, cooling demand for houses and leaving homeowners with less money to spend on all the other things companies want to sell them. Second, as house prices stall, homeowners aren't able to borrow as much against the value of their homes -- a source of cash that has added hundreds of billions of dollars to consumers' spending power in recent years.

"What the Fed is going to do is shut down the ATM machine known as the housing market," says Tad Rivelle, chief investment officer at Metropolitan West Asset Management in Los Angeles. Fed policy makers hold their next meeting on Jan. 31, which is expected to be the last before Chairman Alan Greenspan retires, leaving the reins to Ben Bernanke, the nominee to succeed him.

The Fed's attempts to cool the economy, however, don't always provoke a recession, and many economists, including Mr. Greenspan, suggest that the yield curve might have lost its predictive abilities. That's because foreign buying of U.S. Treasurys and the Fed's success in controlling inflation have kept long-term interest rates unusually low, so U.S. consumers and companies still have relatively cheap access to money that they can spend on buying houses and building factories.

A recent study published by the Fed estimated that in the absence of foreign buying, the difference between two-year and 10-year yields would be about 0.75 percentage point greater.

"Many factors can affect the slope of the yield curve, and these factors do not all have the same implications for future output growth," Mr. Greenspan wrote in a recent letter to Congress.

But even if it doesn't presage recession, a severe and prolonged inversion can cause a lot of pain, particularly for banks and hedge funds that make long-term investments with money borrowed at short-term rates -- the so-called carry trade. Big banks such as Citigroup Inc.'s Citibank unit and J.P. Morgan Chase & Co. have already cited the flattening yield curve as a factor affecting profits, as the interest rate they must pay to attract deposits rises closer to the return they can expect on their investments. "You can't make it up on volume if you're borrowing at 4.25% and lending at 4%," Northern Trust's Mr. Kasriel says.

星期三, 12月 07, 2005

好文章欣賞:陳方安生出來做什麼?

筆陣:梁文道

陳方安生出來做什麼?

正如蔡子強兄所說的,近日香港政局真可說是「波譎雲詭」,相當耐人尋味。尤其值得注意的是十二月四日25萬人爭取普選大遊行之前,先有45條關注組正式組黨,後有陳方安生高調參與遊行,這兩件事對未來的形勢有何影響?二者之間又有沒有聯繫呢?

先談45條關注組在大遊行宣布組黨,從時機上講實在是再對也沒有了。自從「大狀黨」在03年七一大遊行一炮而紅之後,他們可能食髓知味,了解到群眾運動的魅力和造勢的能量,發現遊行原來可以變相地轉換成慶祝組黨的集會。對整個民主運動而言,45條關注組諸君無異於為社會注入了一股形象高潔的清流,可喜可賀。問題只是對於其他民主黨派會不會造成衝擊。

相對而言,45條關注組的弱點之一正是形象太過專業太過高級,略有不食人間煙火之相。且看其公布的成員名單,除了廖銀鳳等少數基層代表之外,恐怕都是平均學歷碩士以上的專業人士。而梁家傑更不諱言在入黨人選的資格上「有要求」,且不忘強調自己「大律師的背景」怎樣影響了理性思維。一不小心,這就容易變成脫離群眾和自高自傲的表現了。試想,如果基層民主派如「阿牛」曾健成等發起大規模入黨運動的話,難道要先考「語文基準試」不成?

好在他們黨團立法會議員裏面還有一向左傾的張超雄,不管這是為了要湊成「關鍵六票」等策略性思維的結果,還是真正的理念相合,到底也是良好信號。兩種情裏面,我寧願相信這是真正的理念同盟,理由是在反對取消遺產稅、爭取最低工資和標準工時等議題上,「大狀黨」都令人驚喜地站在基層的立場。大概是有了從政經驗,接觸到了香港社會的現實。

因此就意識形態而言,45條關注組有傾向社會民主黨的勢頭,同時保留了精英問政的色彩,可說全方面包抄了民主派第一大黨民主黨的路子。相應於此,民主黨該怎麼走下去呢?論中產,是鬥不過45條關注組的了;社會經濟政策向左傾吧,現在的大狀黨也不讓你專美。最可見的道路是緊抓中國軸線,更往支聯會一翼靠攏,以區別開45條關注組和中央政府「有偈傾」的印象。不過對很多民主黨溫和派來說,這條硬派路線或許是個很不現實愈走愈窄的一條路。分析下來,民主黨實在有被「併吞」的機會,反正「大狀黨」也亟待發展基層黨工和地區網絡,民主黨確是個現成好「獵物」。

不料螳螂捕蟬,黃雀在後,一二四大遊行的最大贏家居然是臨時殺出的前政務司長陳方安生。說到這位「香港良心」,我在電台主持節目的時候就曾屢次表達相當有保留的看法,現在也就不怕冒天下之大不韙,再補充幾句。陳方安生出任高官數十年,從未表達過任何追求民主普選的公開言論,更不用說有什麼實際動作。她「香港良心」地位得以確立的轉捩點是與董建華不合,被迫離職。由於當時的董政權幾成香港公敵,凡是敵人的敵人,自然就是家的朋友了。

這數年來,陳方安生不時發表言論,才逐漸成為追求民主的市民的同路人。直到一二四大遊行,其所至之處莫不人頭洶湧,主辦單位要動用十人結成人圈保護她行進,風頭一時無兩,甚至被封上了「民主之母」的稱號。司徒華先生奮鬥數十年方有今日為人敬仰的地位;李柱銘為了爭取民主四處奔波換回一頭白髮,才被稱為「民主之父」;就算劉慧卿也屢戰街頭博回「街卿」的惡罵;如今陳方安生華服錦衣出來遊行了半截,就成了「民主之母」,豈不划算?如果曾蔭權不競選連任,兩年後跑出來爭取中國普選,大概又是「中國良心」了。

饒是如此,當今的政改死結卻只有陳方安生一人能解。以她的精明智慧,選擇在時節出來用一個「普通市民」的身分參與遊行(請注意03年七一遊行針對的是「國安」法律,這回則純粹是香港人自己爭取普選),又有風聲早傳又開記者會,被問及是否重返政壇時又答曰「見步行步」,論者普遍以為她志在千里,甚至有問鼎特首寶座的意思。

但這裏的不通之處有二:一、如果陳方安生要選特首,只有政府的政改方案通過才有機會,拿目前800人選委會的結構來看可謂毫無勝算。二、陳方安生參加遊行,高調表態,豈不是與中央「對幹」?沒有北京的祝福,想當特首可不是難上加難?

所以檢視一下當前形勢。從爭取普選的目標來講,香港人要的是清清楚楚的時間表;但從民主派發展壯大的實際角度來看,政府的政改方案則相當有利。所以泛民主派當初爭取的是修改政府方案,不放委任區議員一關。只是後來形勢逼人,一眾泛民議員被架上道德梁山,最後更與25萬人直奔政府總部。在這個局勢底下,沒有統一領導,各自分散的民主派就算想妥協,也沒有哪一派敢先跑出來給石頭砸。除非有一位「共主」或精神導師適時出現。

當今之世,除了陳日君主教以外,還有誰比陳方安生更有道德地位和號召力呢?且看一二四遊行日,她可說是在驗收「市民的支持與愛戴」,聲勢達到頂。如果政府真有第二方案,如果政府真有一套模糊的路線圖並且去掉委任區議員,陳方安生又願意「無奈」地接受的話,恰巧在此時組黨的45條關注組6席議員該怎麼辦?泛民主派又會不會「顧全大局」?

請留意陳方安生只說爭取普選,只說要有時間表,對於方案本身卻沒有表態否定。又如果她只甘於做民主運動的精神領袖,甚至「傳奇烈士」的話,遊行當日又何不一遊到底直搗黃龍呢?假如陳方安生真能公開接受修改後的政府方案,不只泛民有了轉圜餘地,她能正式就任「民主之母」;就連中央政府也不得不收這份大人情吧!如此一來,民情的支持有了,政改開拓出來的參選空間有了,就連北京的祝福也都拿到半份。水到渠成,誰曰不宜?

接下來則是考驗曾蔭權真正質素的時候了,不讓步的話不只與民為敵,而且也有違情理;讓步的話則等於為自己增添一位連任勁敵。左右如何,甚難決定。

對中央而言,下一屆特首選舉如有全港取得最高民意支持度的兩個人對決,實在是最佳戲碼,哪怕還有「外國勢力」指手劃腳說你不民主?至於我等上過街流過汗的庶民,唯望各方精英以蒼生為念,但願陳太經過民意感動之後也能真真正正地蛻變為民主女神,不要忘記我們這25萬人的赤子之心。

陳方安生出來做什麼?

正如蔡子強兄所說的,近日香港政局真可說是「波譎雲詭」,相當耐人尋味。尤其值得注意的是十二月四日25萬人爭取普選大遊行之前,先有45條關注組正式組黨,後有陳方安生高調參與遊行,這兩件事對未來的形勢有何影響?二者之間又有沒有聯繫呢?

先談45條關注組在大遊行宣布組黨,從時機上講實在是再對也沒有了。自從「大狀黨」在03年七一大遊行一炮而紅之後,他們可能食髓知味,了解到群眾運動的魅力和造勢的能量,發現遊行原來可以變相地轉換成慶祝組黨的集會。對整個民主運動而言,45條關注組諸君無異於為社會注入了一股形象高潔的清流,可喜可賀。問題只是對於其他民主黨派會不會造成衝擊。

相對而言,45條關注組的弱點之一正是形象太過專業太過高級,略有不食人間煙火之相。且看其公布的成員名單,除了廖銀鳳等少數基層代表之外,恐怕都是平均學歷碩士以上的專業人士。而梁家傑更不諱言在入黨人選的資格上「有要求」,且不忘強調自己「大律師的背景」怎樣影響了理性思維。一不小心,這就容易變成脫離群眾和自高自傲的表現了。試想,如果基層民主派如「阿牛」曾健成等發起大規模入黨運動的話,難道要先考「語文基準試」不成?

好在他們黨團立法會議員裏面還有一向左傾的張超雄,不管這是為了要湊成「關鍵六票」等策略性思維的結果,還是真正的理念相合,到底也是良好信號。兩種情裏面,我寧願相信這是真正的理念同盟,理由是在反對取消遺產稅、爭取最低工資和標準工時等議題上,「大狀黨」都令人驚喜地站在基層的立場。大概是有了從政經驗,接觸到了香港社會的現實。

因此就意識形態而言,45條關注組有傾向社會民主黨的勢頭,同時保留了精英問政的色彩,可說全方面包抄了民主派第一大黨民主黨的路子。相應於此,民主黨該怎麼走下去呢?論中產,是鬥不過45條關注組的了;社會經濟政策向左傾吧,現在的大狀黨也不讓你專美。最可見的道路是緊抓中國軸線,更往支聯會一翼靠攏,以區別開45條關注組和中央政府「有偈傾」的印象。不過對很多民主黨溫和派來說,這條硬派路線或許是個很不現實愈走愈窄的一條路。分析下來,民主黨實在有被「併吞」的機會,反正「大狀黨」也亟待發展基層黨工和地區網絡,民主黨確是個現成好「獵物」。

不料螳螂捕蟬,黃雀在後,一二四大遊行的最大贏家居然是臨時殺出的前政務司長陳方安生。說到這位「香港良心」,我在電台主持節目的時候就曾屢次表達相當有保留的看法,現在也就不怕冒天下之大不韙,再補充幾句。陳方安生出任高官數十年,從未表達過任何追求民主普選的公開言論,更不用說有什麼實際動作。她「香港良心」地位得以確立的轉捩點是與董建華不合,被迫離職。由於當時的董政權幾成香港公敵,凡是敵人的敵人,自然就是家的朋友了。

這數年來,陳方安生不時發表言論,才逐漸成為追求民主的市民的同路人。直到一二四大遊行,其所至之處莫不人頭洶湧,主辦單位要動用十人結成人圈保護她行進,風頭一時無兩,甚至被封上了「民主之母」的稱號。司徒華先生奮鬥數十年方有今日為人敬仰的地位;李柱銘為了爭取民主四處奔波換回一頭白髮,才被稱為「民主之父」;就算劉慧卿也屢戰街頭博回「街卿」的惡罵;如今陳方安生華服錦衣出來遊行了半截,就成了「民主之母」,豈不划算?如果曾蔭權不競選連任,兩年後跑出來爭取中國普選,大概又是「中國良心」了。

饒是如此,當今的政改死結卻只有陳方安生一人能解。以她的精明智慧,選擇在時節出來用一個「普通市民」的身分參與遊行(請注意03年七一遊行針對的是「國安」法律,這回則純粹是香港人自己爭取普選),又有風聲早傳又開記者會,被問及是否重返政壇時又答曰「見步行步」,論者普遍以為她志在千里,甚至有問鼎特首寶座的意思。

但這裏的不通之處有二:一、如果陳方安生要選特首,只有政府的政改方案通過才有機會,拿目前800人選委會的結構來看可謂毫無勝算。二、陳方安生參加遊行,高調表態,豈不是與中央「對幹」?沒有北京的祝福,想當特首可不是難上加難?

所以檢視一下當前形勢。從爭取普選的目標來講,香港人要的是清清楚楚的時間表;但從民主派發展壯大的實際角度來看,政府的政改方案則相當有利。所以泛民主派當初爭取的是修改政府方案,不放委任區議員一關。只是後來形勢逼人,一眾泛民議員被架上道德梁山,最後更與25萬人直奔政府總部。在這個局勢底下,沒有統一領導,各自分散的民主派就算想妥協,也沒有哪一派敢先跑出來給石頭砸。除非有一位「共主」或精神導師適時出現。

當今之世,除了陳日君主教以外,還有誰比陳方安生更有道德地位和號召力呢?且看一二四遊行日,她可說是在驗收「市民的支持與愛戴」,聲勢達到頂。如果政府真有第二方案,如果政府真有一套模糊的路線圖並且去掉委任區議員,陳方安生又願意「無奈」地接受的話,恰巧在此時組黨的45條關注組6席議員該怎麼辦?泛民主派又會不會「顧全大局」?

請留意陳方安生只說爭取普選,只說要有時間表,對於方案本身卻沒有表態否定。又如果她只甘於做民主運動的精神領袖,甚至「傳奇烈士」的話,遊行當日又何不一遊到底直搗黃龍呢?假如陳方安生真能公開接受修改後的政府方案,不只泛民有了轉圜餘地,她能正式就任「民主之母」;就連中央政府也不得不收這份大人情吧!如此一來,民情的支持有了,政改開拓出來的參選空間有了,就連北京的祝福也都拿到半份。水到渠成,誰曰不宜?

接下來則是考驗曾蔭權真正質素的時候了,不讓步的話不只與民為敵,而且也有違情理;讓步的話則等於為自己增添一位連任勁敵。左右如何,甚難決定。

對中央而言,下一屆特首選舉如有全港取得最高民意支持度的兩個人對決,實在是最佳戲碼,哪怕還有「外國勢力」指手劃腳說你不民主?至於我等上過街流過汗的庶民,唯望各方精英以蒼生為念,但願陳太經過民意感動之後也能真真正正地蛻變為民主女神,不要忘記我們這25萬人的赤子之心。

星期一, 11月 28, 2005

大白象

"white elephant" came, in English, to mean a thing which is more trouble than it is worth, or has outlived its usefulness to the person who has it.

A list of white elephants

The term was coined after New York Giants manager John McGraw told the press that Philadelphia businessman Benjamin Shibe had "bought himself a white elephant" by acquiring the Philadelphia Athletics baseball team in 1901, A's manager Connie Mack selected the elephant as the team symbol and mascot. The team is occasionally referred to as the White Elephants.

Other examples include:

A list of white elephants

The term was coined after New York Giants manager John McGraw told the press that Philadelphia businessman Benjamin Shibe had "bought himself a white elephant" by acquiring the Philadelphia Athletics baseball team in 1901, A's manager Connie Mack selected the elephant as the team symbol and mascot. The team is occasionally referred to as the White Elephants.

Other examples include:

- Aircraft:

- Concorde, a supersonic transport built by Aérospatiale and BAC, intended to allow high-speed intercontinental travel. Only fourteen examples saw service, though development costs were to be amortized over hundreds of units.

- Bristol Brabazon, an airliner built by the Bristol Aeroplane Company in 1949 to fly a large number of passengers on transatlantic routes from England to the United States.

- The U.S. Space Shuttle is also considered an example of a white elephant, as its continued existence is debated versus other forms of space transportation, which are thought by some to be more reliable and affordable.

- The Hughes H-4 Hercules, or "Spruce Goose," was often called Howard Hughes's white elephant before and during Senate War Investigating Committee

- Railway:

- The fully automated North East Line and Bukit Panjang LRT Line struggle to break even by their operators.

- Structures and engineering projects:

- Kansai International Airport, located on an artificial island in Osaka Bay, south of Osaka, Japan, is considered an example of a white elephant, as it was constructed largely as a matter of pride, and though at a fraction of nominal capacity, is being doubled in size.

- Montréal-Mirabel International Airport, a large airport located in Mirabel, Quebec, near Montréal.

- Superconducting Super Collider (or SSC), a large particle accelerator which was being constructed in Texas. Billions of dollars had been spent on the project by the time of cancellation, and the project termination itself cost hundreds of millions of dollars.

- Three Gorges Dam, a monumental project to bring hydroelectric power to the Yangtze River basin in China, beset with construction and environmental issues.

- World Trade Center México, a building complex located in Mexico City, Mexico, a building and complex that never really performed their intended functions and were known as a white elephant which eventually bankrupted their owners without ever being finished.

- Technology:

- Intel's IA-64 (better known as Itanium) (semiconductor architecture), which cost billions of dollars to develop, now relegated to a niche role in the computer industry. See also Itanic.

- Nautical:

- SS Great Eastern, a ship designed by Isambard Kingdom Brunel. She was the largest ship ever built at the time of her launch, and had the capacity to carry 4,000 passengers around the world without refuelling.

WHAT is the meaning of Xbox?

WHAT is the meaning of Xbox?

Its name has horribly geeky origins: the bit of Microsoft's Windows software that does fancy graphics is called DirectX, so when the company moved into games consoles in 2001, it wanted a “DirectX box” that was optimised for graphical performance.

Its name has horribly geeky origins: the bit of Microsoft's Windows software that does fancy graphics is called DirectX, so when the company moved into games consoles in 2001, it wanted a “DirectX box” that was optimised for graphical performance.

泰國也有領匯事件

Fermenting trouble

Nov 24th 2005 BANGKOK

From The Economist

The unsettling effect of shelving two share offerings

DRIVING past the Stock Exchange of Thailand, you never know what you might see. A few months ago, orange-robed Buddhist monks were protesting against the planned listing of Thai Beverages, the country's biggest brewer and distiller. More recently, left-wing activists marched against the partial privatisation, through a public offering, of Egat, the state-owned electricity monopoly. Indeed, these days, demonstrators seem more interested in Thai stocks than investors are.

In 2003 Thai stocks were among the world's top performers. The main market index more than doubled, as the economy grew by 6.9% and finally shook off the torpor that had set in after the crash of 1997. Alas, Thailand has since suffered a string of misfortunes: bird flu, last year's tsunami, a prolonged drought and an intensifying insurgency in some Muslim areas. Meanwhile, dearer oil has pushed inflation up, prompting the central bank to raise interest rates repeatedly. Expensive oil imports have also weighed on the current account, and so on the baht.

In the first quarter of this year, the economy even shrank slightly. Over the whole year, it might grow by some 4%, far less than optimists had expected. In August consumer confidence hit its lowest in three years. All this gloom has affected share prices too. The market looks like ending the year where it began, 15% below the peak it reached early last year.

The protests have not helped. The listing of Thai Beverages, originally scheduled for the middle of the year, would have been the biggest-ever flotation of a private Thai firm, worth roughly 40 billion baht ($980m). But the World Health Organisation ranks Thais as the world's fourth-keenest drinkers, and temperance groups, supported by Buddhist clergy, argued that the listing would foster further boozing. The stock exchange and its regulator have not yet dared approve it.

The government's attempt to sell a stake in Egat has dragged on even longer. It first postponed the offering last year, after protests by the company's staff. As a sweetener, it raised workers' salaries and reserved shares for them, before reviving the sale earlier this year. It had planned to sell 25% of Egat this month, for 33 billion baht or so. But at the last minute, a court put the listing off again, to consider activists' charge that the decree authorising the sale violates the constitution. The government still hopes that the sale, and the rest of its privatisation programme, will go ahead—but the court has not even set a date for a ruling.

On the other hand, Thai stocks now look cheap next to other markets in the region, or at any rate cheaper than they did. The average price/earnings ratio, which topped 14 in 2003, is now around nine, and falling. If, as economists expect, the recent easing of the oil price continues next year, and interest rates also decline, the market should start to recover. And the resuscitation of the shelved listings might give traders cause to celebrate—soberly, of course.

Nov 24th 2005 BANGKOK

From The Economist

The unsettling effect of shelving two share offerings

DRIVING past the Stock Exchange of Thailand, you never know what you might see. A few months ago, orange-robed Buddhist monks were protesting against the planned listing of Thai Beverages, the country's biggest brewer and distiller. More recently, left-wing activists marched against the partial privatisation, through a public offering, of Egat, the state-owned electricity monopoly. Indeed, these days, demonstrators seem more interested in Thai stocks than investors are.

In 2003 Thai stocks were among the world's top performers. The main market index more than doubled, as the economy grew by 6.9% and finally shook off the torpor that had set in after the crash of 1997. Alas, Thailand has since suffered a string of misfortunes: bird flu, last year's tsunami, a prolonged drought and an intensifying insurgency in some Muslim areas. Meanwhile, dearer oil has pushed inflation up, prompting the central bank to raise interest rates repeatedly. Expensive oil imports have also weighed on the current account, and so on the baht.

In the first quarter of this year, the economy even shrank slightly. Over the whole year, it might grow by some 4%, far less than optimists had expected. In August consumer confidence hit its lowest in three years. All this gloom has affected share prices too. The market looks like ending the year where it began, 15% below the peak it reached early last year.

The protests have not helped. The listing of Thai Beverages, originally scheduled for the middle of the year, would have been the biggest-ever flotation of a private Thai firm, worth roughly 40 billion baht ($980m). But the World Health Organisation ranks Thais as the world's fourth-keenest drinkers, and temperance groups, supported by Buddhist clergy, argued that the listing would foster further boozing. The stock exchange and its regulator have not yet dared approve it.

The government's attempt to sell a stake in Egat has dragged on even longer. It first postponed the offering last year, after protests by the company's staff. As a sweetener, it raised workers' salaries and reserved shares for them, before reviving the sale earlier this year. It had planned to sell 25% of Egat this month, for 33 billion baht or so. But at the last minute, a court put the listing off again, to consider activists' charge that the decree authorising the sale violates the constitution. The government still hopes that the sale, and the rest of its privatisation programme, will go ahead—but the court has not even set a date for a ruling.

On the other hand, Thai stocks now look cheap next to other markets in the region, or at any rate cheaper than they did. The average price/earnings ratio, which topped 14 in 2003, is now around nine, and falling. If, as economists expect, the recent easing of the oil price continues next year, and interest rates also decline, the market should start to recover. And the resuscitation of the shelved listings might give traders cause to celebrate—soberly, of course.

星期五, 11月 18, 2005

Copper trader missing

Crouching trader, leaping prices

Nov 17th 2005

From The Economist

How a big bad bet is pushing up the price of copper

ALL that remains is to sell the film rights. Liu Qibing, a trader handling China's strategic commodity reserves, allegedly shorted the vast quantity of 100,000-200,000 tonnes of copper, then vanished when prices moved against him. The stuff of latter-day legend, this briefly pushed an already upwardly mobile market into near-vertical ascent.

“Shorting” a commodity involves borrowing the commodity itself and selling it to someone else with the intention of buying more later to return to the lender. A trader only does this when he believes, with some confidence, that prices will fall. Since copper has gained more than 30% this year and more than 200% since 2003, it is reasonable to think it due for a drop. Plenty of other traders and speculators have bet that way too.

But the metal is not obliging them. The three-month contract on the London Metals Exchange (LME) was already trading at record levels on November 11th, closing at $4,105 per tonne. When the tale of Mr Liu broke on November 14th, rousing expectations that China would have to buy a lot of the red stuff to meet commitments, it closed $20 per tonne higher. Copper hit a new record price of $4,174 on November 15th, and moved higher still on November 17th.

Mr Liu's copper is due for delivery to LME-approved warehouses in December. Will it be there? China claimed last week to have 1.3m tonnes of the metal stockpiled, far more than most western analysts reckon it has. This week, it held its first copper auction ever, selling 20,000 tonnes and pledging to unload more on November 23rd. And there is talk that the State Reserve Bureau, for which Mr Liu was acting, has applied to export 200,000 tonnes this year.

But this all sounds more like deliberate market-cooling before a purchase than like a surfeit of supply. Copper is scarce these days. Years of commercial underinvestment, together with work stoppages that grew more bitter as the copper price rose, have kept a lid on worldwide output. Last week Chile, the largest producer by far, lowered its output targets for 2005 and 2006.

Demand, meanwhile, was booming, until this year. And in fast-growing China, now the world's largest copper user, it is still increasing by leaps and bounds. The usual cushions of inventory and spare capacity have vanished: global stocks are depleted, as the chart shows. Mining companies should respond to this by investing in increased production. But the results will come, if at all, some years down the track.

The fall-out from Mr Liu's speculation-gone-wrong is hard to judge. If he assumed his positions last spring, as some suggest, when copper prices were below $3,300 per tonne, it is possible that the losses now amount to $200m.

But more than money may be at stake. China was expected to liberalise its derivatives markets a touch next year. After this bruising brush with those outside, it may be disinclined to do so.

Nov 17th 2005

From The Economist

How a big bad bet is pushing up the price of copper

ALL that remains is to sell the film rights. Liu Qibing, a trader handling China's strategic commodity reserves, allegedly shorted the vast quantity of 100,000-200,000 tonnes of copper, then vanished when prices moved against him. The stuff of latter-day legend, this briefly pushed an already upwardly mobile market into near-vertical ascent.

“Shorting” a commodity involves borrowing the commodity itself and selling it to someone else with the intention of buying more later to return to the lender. A trader only does this when he believes, with some confidence, that prices will fall. Since copper has gained more than 30% this year and more than 200% since 2003, it is reasonable to think it due for a drop. Plenty of other traders and speculators have bet that way too.

But the metal is not obliging them. The three-month contract on the London Metals Exchange (LME) was already trading at record levels on November 11th, closing at $4,105 per tonne. When the tale of Mr Liu broke on November 14th, rousing expectations that China would have to buy a lot of the red stuff to meet commitments, it closed $20 per tonne higher. Copper hit a new record price of $4,174 on November 15th, and moved higher still on November 17th.

Mr Liu's copper is due for delivery to LME-approved warehouses in December. Will it be there? China claimed last week to have 1.3m tonnes of the metal stockpiled, far more than most western analysts reckon it has. This week, it held its first copper auction ever, selling 20,000 tonnes and pledging to unload more on November 23rd. And there is talk that the State Reserve Bureau, for which Mr Liu was acting, has applied to export 200,000 tonnes this year.

But this all sounds more like deliberate market-cooling before a purchase than like a surfeit of supply. Copper is scarce these days. Years of commercial underinvestment, together with work stoppages that grew more bitter as the copper price rose, have kept a lid on worldwide output. Last week Chile, the largest producer by far, lowered its output targets for 2005 and 2006.

Demand, meanwhile, was booming, until this year. And in fast-growing China, now the world's largest copper user, it is still increasing by leaps and bounds. The usual cushions of inventory and spare capacity have vanished: global stocks are depleted, as the chart shows. Mining companies should respond to this by investing in increased production. But the results will come, if at all, some years down the track.

The fall-out from Mr Liu's speculation-gone-wrong is hard to judge. If he assumed his positions last spring, as some suggest, when copper prices were below $3,300 per tonne, it is possible that the losses now amount to $200m.

But more than money may be at stake. China was expected to liberalise its derivatives markets a touch next year. After this bruising brush with those outside, it may be disinclined to do so.

訂閱:

文章 (Atom)